Family finances don’t have to be intimidating. Check out these tips on how to talk to your spouse about money without fighting and watch all your big dreams begin to unfold!

A quick google search will reveal a plethora of articles that relate finances to being one of the top reasons for divorce. The surprising thing is that it isn’t just a lack of money that causes this rift. You can be swimming in money and still have problems; it’s the tension around differing money views and habits. Of course we are all going to come into a marriage with financial beliefs and practices that differ from our partners, but if we want a happy marriage we need to make creating common financial goals and talking through spending habits a top priority.

That sounds easy enough, right? It’s not always. Money is an emotional topic because it is tied to almost every aspect of life. Add in the factor that one partner might be a spender, and the other a saver, and without great communication, the result is a turbulent situation.

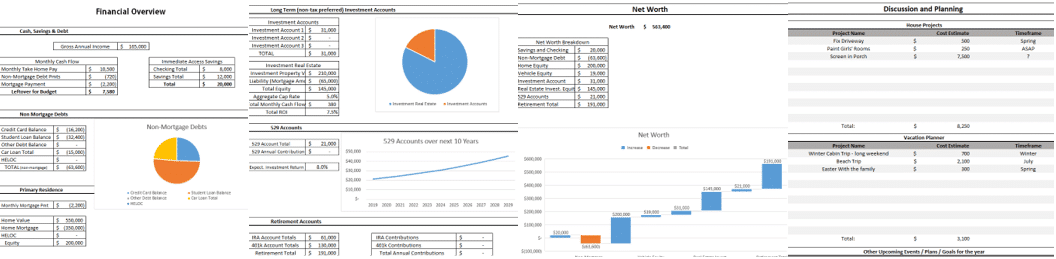

We need to be on the same page as our spouse on finances. We need to know where the money comes from, where it goes, how much we have, where that money is located, and how much we will have down the line. It was these goals that originally inspired David to create The State of the Family a decade ago, at the beginning of our marriage. He is the more naturally finance-minded one in our union, and he wanted to ensure we both not only understood our finances, but were aligned with a common vision as to where we were headed in life, and therefore with our savings and investments as well.

How to Talk to Your Spouse About Money Without Fighting

Start with the dreamer conversation.

Discussing finances sounds so serious. While it is really important stuff, it doesn’t mean it has to be boring or stiff. After all, money in and of itself is not all that important; what you can do with that money is. Money, after all, is just a tool. Starting with a conversation about your big dreams in life is so important because it aligns your vision and provides you both with a strong why to hold on to when the process might become not-so-fun. This conversation should take place when you are both relaxed and in a good mood. Ideally when the kids (if you have kids) aren’t hanging on your leg.

Start by asking each other those common dating questions. For example: where do you see us in five, ten, and fifty years? If you had a million dollars in your pocket today, what would you do with it? Now go deeper into those- what does life truly look like for us in 10 years- where do we live? What are the kids doing? How do we spend our weekends? Where are we working? How often do we vacation? Where do we vacation? Are we involved in charities? To what level are we involved? So on and so forth.

Again, there is no wrong answer here and keeping this conversation exciting and fun is key. This is not the time to scoff as your partner’s big dream of wanting to own a banana stand on a beach. Jump into that fantasy with them, explore it, laugh. Start noticing which goals are most important to you both and write those down. What goals do you have in common? What excites you both about the future? Write these down, make a vision board, tattoo them on your wrist- you do you.

Print out an overview of your current financial situation.

Again, this is why I can’t recommend The State of the Family worksheets enough. They will hold your hand and walk you through all the numbers you should be paying attention to from your current spending, to how much you have in the bank, in investments, in tax-preferred savings accounts, etc. It also will show you your net worth, which is a number worth tracking over the years. Can you do all of this without the worksheets? Absolutely. I don’t care how you do it, but it’s an essential part in getting on the same page with your partner about your current financial situation, so figure out the way that works best for you.

Traditionally for us, David does all the number hunting and filling out the forms, then we find a time to sit down and go over it line by line together. This allows him to nerd out on Excel (his love language) and I don’t get worn out hunting for bank log in passwords before the process even begins.

Going over your current financial situation is usually not as uplifting as the dreamer conversation, but it’s OK. With annual repetition, it actually will be, as you watch your net worth grow. However, until that happens, this step can bring up a lot of emotion. It’s vitally important that neither partner assigns blame to the other during this process. In fact, agree on that ahead of time and pick a time to do this when you are both in the right frame of mind. Remember, it’s not her student debt; if you are married, it is both of your student debt. It’s not his income; it’s your combined household income. You two are a team and you take on your finances as a team.

Create a common short term goal.

I love Dave Ramsey’s approach to debt because he highlights the fact that money is emotional and to use that to your advantage (which is why he recommends paying off debts smallest to largest, not in order of interest rate). To get the excitement about tackling money together rolling, you need to unite behind a common, achievable, short-term goal. Maybe that’s paying off a credit card or getting $1000 in an emergency fund or saving up to pay cash for your annual beach trip.

Once you choose one short term goal (stick to just one for now), write it down and put it in a place you both can see it daily so you are reminded by it. Then, choose a reward you both will enjoy once you reach that goal. For us, a nice date night out does the trick (I love you, Kindred!). Then make it into a game! Go after that goal together with intensity but with a playful attitude. When you are tackling a common goal together, it makes it fun. You’ll get excited to show him how you shaved $20 off the food budget to put towards the goal or maybe how you picked up a freelance project to throw an extra couple hundred at it.

Decide who is responsible for what

While it’s important to have the team approach to finances in general, it’s also fine and good to divide up the responsibilities. Pick who will pay the bills, who will deposit checks, who has the venmo account set up for paying the sitter, etc. In our marriage I found that I naturally enjoy and thrive in managing the micro tasks (budgets and bill pay) while David is best suited for monitoring the macro (investment accounts, rental properties, etc). Remember that this is still a joint venture and transparency is a given, but it’s just easier to implement day to day living with tasks clearly assigned.

Create a budget

We give you a simple monthly budget sheet in The State of the Family workbook, but there is no inherit magic in it because there are a million ways to create a budget. If you are new to budgeting, I highly recommend just tracking your spending, every dollar, for a month or two, then creating a budget based on your real spending. It will make it more realistic. Remember, the goal with budgeting is not necessarily to lower the amount you spend in every category, but just to have an accurate and clear picture of where your money is going. We’ve found it most helpful to divide monthly expenses into two categories: discretionary (Starbucks, groceries, clothes) and non-discretionary (mortgage, insurance, etc) so we can more easily see which categories we can have more control over.

Create a vision board of your big goal

By this point in the process things can be feeling less fun and sometimes even a little heavy and draining. Now is the time to remind you both of why you are doing all of this. Rallying behind your common goal is the best way to maintain commitment and momentum towards your financial goals. Remember that dream life you came up with together? Write it down, draw it out, rip pages out of magazines and tape them to your mirror (yes, we did this one), make the image your computer or phone background. Put the big goal where you both can see it. Then remember to talk about it and envision it weekly. You’ll need to be united behind your why when the urge comes to buy the kids yet another pair of expensive, organic, matching pajamas (…yup, talking from experience here).

Remember… to be successful in discussing money with your partner it’s important to:

- not assign blame. You are a team and you spend and save as one.

- understand that you both are approaching money from different backgrounds and therefore might have different views and motivations. That’s expected and OK; the goal is to create commonality and get on the same page with the big goals.

- talk to each other often about money (but not when one partner is overtired or stressed). David and I check in weekly, even if it’s just briefly, to chat about where money is coming from and where it’s going, surprise expenses, etc.

- celebrate your financial wins. You have to stay motivated and celebrating along the way is key to maintaining longevity in going after your goals.

- seek a financial coach or adviser. It’s wonderful to have an outside, knowledgeable opinion bounce ideas off of and get another opinion.

Did you enjoy the topic of how to talk to your spouse about money without fighting? We discuss these topics and many others live on video each week in our State of the Family Facebook group, which you get free access to when you purchase The State of the Family workbook. If you are interested in getting serious about your finances and planning big goals to create your vision of an incredible life, we’d love you to join us!

John J. Stathas says

Great article about one of the big 3 of divorce causers, along with sex and kids. Your pragmatic team approach is a good guide for everyone to check into how they manage money in their respective household. You guys are good role models and teachers! Your State of the Family package is truly timely and helpful.